Cash Flow Was the Last Edge. Defending What You Deploy Is the Next One.

- Aditya Khandekar

- Jun 11

- 4 min read

Cash flow underwriting delivered what it promised. Approval rates improved on thin-file applicants without a corresponding rise in charge-off. The regulatory path became navigable. The tools proliferated, costs fell, and adoption ran its course.

That adoption also opened a model risk surface that most institutions have not fully audited. Every alternative data source embedded in a credit model since 2020 carries model governance obligations under SR 11-7 and fair lending exposure under ECOA and Regulation B. As institutions evaluate what comes after cash flow, the risk question is not whether the next data type works. It is whether the institution can defend it to an examiner — on its own loan file, not a vendor’s curated benchmark.

The institutions building durable underwriting advantages in this environment are not simply adopting more data. They are sequencing deployment by governance readiness and knowing, with precision, which categories carry examination risk they cannot yet resolve.

Four Data Categories. Four Different Risk Profiles.

The next wave of alternative underwriting data is not a single category. It is four distinct data types at different stages of technical readiness, regulatory maturity, and fair lending exposure. Treating them uniformly is how institutions end up either overexposed on compliance or competitively underbuilt. The distinction matters more than most vendor conversations acknowledge.

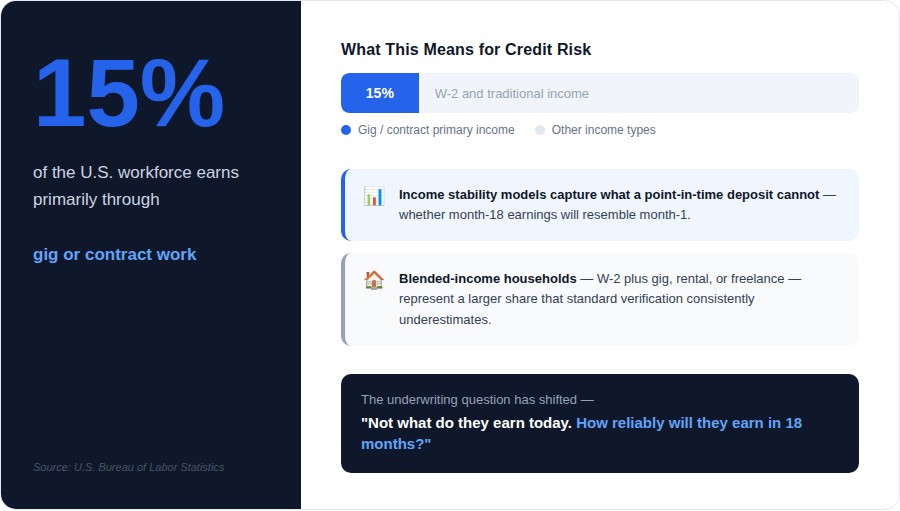

Income stability scoring distinguishes what a member earns from how reliably they earn it. According to the Bureau of Labor Statistics, 15 percent of the U.S. workforce engages in independent contract work as a primary income source, a figure that understates the larger share of households supplementing W-2 income with gig, rental, or platform earnings. A point-in-time deposit does not model month-18 income reliability. A longitudinal volatility model does.

Verdict: The regulatory path is navigable today.

Real-time liquidity buffer modeling addresses the gap between application-date balance and payment-date capacity. A member carrying $2,000 at application may have $200 when payment falls due if rent auto-drafts in the intervening 72 hours. A member with $800 at application may have $1,400 because their direct deposit cycles two days prior.

Verdict: Balance is not the risk variable. Velocity is. Requires robust open banking infrastructure.

Household income diversification is an 18-to-24-month horizon. The data infrastructure is maturing, not deployed. Begin vendor conversations now; do not commit capital to production deployment next quarter.

Verdict: The data infrastructure is developing. Worth preparing for, but not ready for production at scale.

AI-exposure data by employer and industry carries the highest regulatory risk in the category, which the next section addresses directly. This refers to models that assess how vulnerable a borrower’s job or industry is to automation, and use that as a proxy for future income stability.

Verdict: Do not deploy until examiner posture clarifies.

The Examination Will Ask What the Vendor Pitch Did Not.

Every vendor in this space will show lift. The backtest will be clean. The approval rate improvement will be real, in the vendor’s test population, under the vendor’s conditions, against a dataset the vendor curated.

What the pitch deck will not show is a disaggregated fair lending analysis run against this institution’s own loan file: actual approval and denial rates by race, gender, and age drawn from the institution’s own member portfolio.

ECOA and Regulation B create liability for models that produce disparate impact against protected classes, even when the input data is facially neutral. AI-exposure data by employer and industry carries the sharpest risk in this dimension. Certain protected classes are statistically overrepresented in high-automation-exposure occupations. A model that penalizes those occupations will produce disparate impact patterns; a fair lending examination will surface, regardless of the economic validity of the signal.

SR 11-7 model risk management expectations compound the exposure. They apply to alternative data models the same way they apply to any credit scoring model: the institution must be able to explain outputs to an examiner and to an adverse action notice recipient. Explainability for AI-exposure implementations is largely unresolved. That is not a reason to dismiss the signal. It is a reason to keep it in the watch column until it is.

The institutions building durably are treating regulatory defensibility as an upstream design requirement, not a retrofit. Governance built before deployment is a competitive advantage. Governance built in response to an examination finding is an incident report.

Sequencing Is Risk Management. The Portfolio Posture That Follows.

'

Let's take a look at an example.

Institution A is a $4 billion credit union in the Midwest. It leads with income stability scoring and real-time liquidity buffer modeling, both available today, both with navigable fair lending defensibility when tested against the institution’s own member file. It builds model performance history now, so that when household income diversification data matures in 2027, it enters that deployment with 18 months of validated, documented experience on adjacent capabilities already in hand.

Institution B is a $3.5 billion community bank in the Southeast. It deploys an employer AI-exposure score without first running a disaggregated fair lending analysis on its own loan file. The backtest lifts. Eighteen months later, an examination flags disparate impact in denial rates for applicants in manufacturing-heavy zip codes. The difference between these two institutions is not analytical sophistication. It is not a budget. It is whether governance was a design requirement or an afterthought.

Income stability scoring and liquidity buffer modeling belong in the no-regret column. Household diversification belongs in build-optionality - begin the vendor and permissioning work now, target 2027. AI-exposure data stays in the watch column until CFPB and OCC examiner posture establishes itself. The competitive differentiator will not be who signed the

vendor contract first. It will be who has two years of through-cycle model performance data, validated against their own portfolio, before the rest of the market has started building.

What distinguishes Institution A is the validation and testing infrastructure that backs it along with the sequence decisioning. Running a new data signal against the institution’s own portfolio, stress-testing it across economic scenarios, monitoring performance as conditions shift: that work happens before deployment, not in response to an examination finding. Credit union service organizations focused on decisioning infrastructure, such as Precision CUSO, are building precisely this capability, model validation and testing environments that let credit unions evaluate signals against their own member data rather than relying on a vendor’s curated benchmark.

The question is not which vendor demo was most compelling last quarter, or which data category shows the best lift in a controlled backtest. The question is a governance audit of what is already deployed.

We would welcome a conversation about how your institution is thinking through it.

Comments